The REIT Footprint Expands Globally

Global Trends in Listed Real Estate

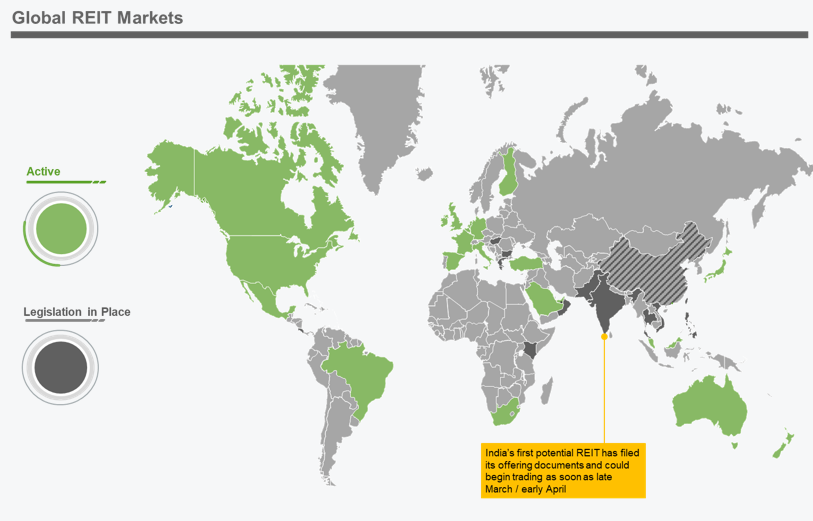

REIT markets around the globe have seen immense growth in recent years. The cumulative market capitalization of REITs globally is approaching $2 trillion, as 35 countries now have active REIT legislation, including 25 nations with at least one actively traded REIT. The next wave of growth is likely to be driven by non-traditional property sectors in the mature U.S. and European markets and the emergence of listed real estate sectors in high-growth Asian markets.

The U.S. REIT market has been fundamentally transformed over the last three decades due to the growth of non-traditional real estate sectors. Newer property types, such as self-storage, health care, cell towers, and data centers now comprise over half of the total U.S. REIT market capitalization. In recent years, the growth in publicly listed REITs focused on core sectors – apartments, industrial, office, and retail – has been muted by suppressed capital markets activity driven by discounts to net asset value and slow property price appreciation. In contrast, non-traditional REITs have benefited from stronger asset price appreciation and a favorable cost of capital in the public market, leading to more capital market activity including IPOs. Non-traditional sectors continue to attract capital, perform well on a total return basis relative to traditional sectors, and are becoming a bigger piece of the pie in the U.S. REIT market. See Green Street’s report on recent Commercial Property Price Index enhancements for more information about the tremendous growth in non-traditional sectors over the past decade.

Emerging non-traditional sectors represent an opportunity in the U.K. and Continental Europe, where the listed market has been dominated by traditional sectors. In October 2018, Public Storage (PSA), the owner of a $36 billion U.S. self-storage portfolio, filed an IPO for its European platform under the name Shurgard Self Storage (SHUR (EBR)), creating the first self-storage REIT in continental Europe. Green Street expects more non-traditional IPOs to emerge over the next few years.

In Asia, several markets are poised for growth. India recently completed final revisions on its legislation for REITs, and although the first REIT has yet to be established, there has been significant buy-in from market participants. Green Street’s Advisory Group spent time in India over the past twelve months and witnessed the palpable excitement for the coming REIT market. Recent reporting suggests the launch of India’s first REIT is imminent with deal execution scheduled for late March 2019 and trading scheduled to begin in early April 2019. Singapore, with its REIT market cap approaching $70 billion USD, also merits attention. Interestingly, most Singapore-listed companies own assets outside of the country. That makes Singapore’s REIT market a unique avenue for real estate owners around the globe to list on a public exchange and access new investors, including high net worth and institutional investors in Asia.

Opportunity Grows in India

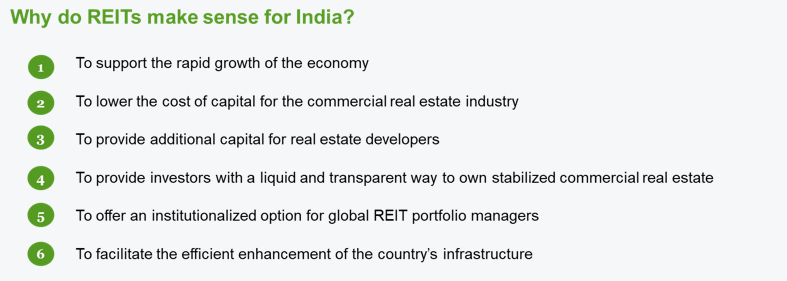

India’s nascent REIT regime is expected to offer domestic and international public-market investors the opportunity to invest in stabilized institutional-quality real estate in India for the first time. The real estate companies currently listed on the Indian stock exchange are primarily condominium developers that have seen boom-and-bust cycles and offer a very different risk profile than the stabilized real estate of REITs. The relative stability of income from REIT property portfolios will likely find a home in the investment portfolios of domestic insurance companies, pension funds, and mutual funds over time.

The quickly growing supply of institutional-quality real estate in India, particularly in the office sector, has attracted many of the largest private equity firms and sovereign wealth funds to the private market over the past five to seven years. The first REITs are likely to come from the office sector with a focus on large technology park properties. These office portfolios have been the primary target of global institutional capital in the private market due to their strong combination of tenant credit, current yield, and rent growth prospects. The hope is that the REIT market will further expand this investment opportunity to a broader base of public market investors. From a global perspective, REITs in India will offer international investors, whether real-estate focused or generalists, direct exposure to real estate in the fastest-growing large economy in the world.

Cross-Border Valuation Challenges

Properly assessing relative value between REITs and property sectors across borders is challenging. It is wise for global investors to keep several key considerations top-of-mind.

The first is corporate level taxation. REITs in the United States are pass-through entities, meaning they do not pay corporate-level tax. This structure has been widely adopted globally, but it is not universal. There is some level of corporate taxation in certain markets, especially where REITs own assets outside of the country in which they are listed.

The second consideration is capital expenditures (cap-ex). When evaluating companies in the United States within the same sector, there is typically a tight range of required cap-ex. Once investors cross international borders, those ranges widen materially. The best example of this is in the office space. In the U.S. office sector, Green Street estimates that cap-ex eats up about 30% of net operating income (NOI), and a majority of that is leasing costs such as tenant improvements and leasing commissions. In some Asian markets by contrast, including India, the tenant is responsible for the build-out improvements. This arrangement leads to a very different and more attractive cap-ex profile for office landlords in those markets.

The final area to consider is sovereign risk. How much additional return should REIT investors require to invest in an identical asset in India versus one in the United States? To answer this question, Green Street looks to sovereign debt yields as a guide; more specifically, the spread between the unlevered total return expected from the REITs at their current pricing and the sovereign debt yield in that market. All things being equal, a wider positive spread indicates more attractively priced REITs on a relative basis. A question worth consideration is how much a strong multi-national tenant credit profile should offset the sovereign risk.

Recommendations for Emerging Market REITs

While investors evaluating cross-border opportunities face challenges, the emerging market REITs seeking global capital also experience unique challenges. Green Street’s Advisory Group works with REITs trying to broaden their investor bases, private companies looking to enter the REIT market via IPOs, and C Corps seeking to enter the market through REIT conversions. These types of clients benefit from independent and expert support in messaging, disclosure, and corporate governance in order to be best received by the REIT-dedicated investment community. In emerging markets, those challenges can be magnified.

Corporate governance is a key area of focus for global REIT fund managers. Many markets in Asia have adopted an externally-managed structure, which is not the preference of Green Street or REIT-dedicated investors in the United States. Most U.S. REIT investors believe an internal structure creates a better alignment of shareholder and management interests. Because of this, emerging market REITs that are externally advised should go above and beyond historical norms when designing external management contracts. In particular, it’s important to contractually align the interests of the external manager and the public market shareholders wherever possible, and to ensure the total management fee is comparable to the general and administrative expenses (G&A) load at a comparable internally managed company.

Emerging market REITs should also place a strong emphasis on financial disclosure when preparing to attract global investors. It can be difficult for investors to make apples-to-apples comparisons across borders because of the different accounting standards and different free cash flow metric definitions. It is critical for emerging market REITs to translate their performance metrics to those that global REIT investors know well.

Green Street believes the securitization of real estate is a powerful trend that will continue, and the growing REIT market around the world offers exciting new opportunities and challenges. With dedicated advisory professionals in the U.S. and Europe serving clients spanning five continents, Green Street's Advisory Group is uniquely positioned to translate real estate best practices across global markets.

*Update: Embassy Office Parks REIT successfully completed the first REIT IPO in India in March 2019. Green Street's Advisory & Consulting Group was a strategic advisor on the deal.

Related Resources:

- Blog: Non-Core Sectors Come of Age, CPPI Expanded

- Webinar: Cross-Atlantic Considerations for Real Estate Investors

- Video: Best Practices for Small Companies Competing for Capital

- Green Street Advisory Group White Paper: Mall Tenant Turnover Analysis

Learn more about our insights

Our thought leadership helps thousands of clients make better investment decisions every day. Inquire here to learn more about Green Street’s product suite.

More Stories

ESG and Climate Change

Energy In The Economy: Energy Is The Economy

Investment Strategy

Opportunities to Be Thankful for In the Current Market

Video