Apartments: Bright Spots and Warning Signs

Underlying Opportunity

Apartment investors in the public market are more skeptical of the outlook for asset values and net operating income (NOI) growth than their counterparts in the private market. Since the selloff in REITs earlier this year, apartment REITs have been trading at a significant discount to net asset value (NAV), meaning that the public market is pricing real estate below the underlying private-market value of these assets. Green Street sees apartment sector-specific headwinds on the horizon, including slowing employment growth, rising homeownership, new supply, and demographic shifts, but finds opportunity in the disconnect in public and private pricing for investors heeding the signals. Despite demographic and supply trends that bear watching, risk-adjusted returns for the apartment sector are favorable compared to all other major property types.

Fundamental Backdrop

Green Street’s employment growth forecasts are a key starting point for assessing apartment fundamentals. The relationship between annual job growth and rent growth is strong. With the economy near full employment, the recent job growth pace of 200,000 jobs per month will become increasingly tougher to meet and job growth should decelerate in coming years. Tax cuts should provide a slight boost to 2018 employment growth, but with only minimal impact in later years.

Average Nonfarm Monthly Job Growth Pace (000's)

Green Street’s near-term forecast for market occupancy and rent changes – as measured by market revenue per available foot (M-RevPAF) – is for inflation-like growth, well below the projections from other third-party data providers. The residential team’s forecast, built from a top-down macro-level and bottom-up market-level perspective, predicts more moderate employment gains, steady supply growth, and a bottoming of the homeownership rate.

Rising Homeownership

Household formations have accelerated in 2018 from 2017’s lackluster pace, but homeowners, and not renters, have accounted for most of the growth. While household formation trends are best viewed over longer periods, renter household formation is trending well below our expectations.

As a consequence, the U.S. homeownership rate improved in 2017 and early 2018, following a bottoming in 2016, and Green Street recently raised its near-term homeownership rate forecast. The volatility of quarterly census data on homeownership warrants caution, but the recent trajectory indicates: 1) The desire to own a home is still alive and well, and 2) The ability to own, particularly among key renter cohorts, is clearly improving though restrained versus historical levels.

Fading Demographic Tailwind

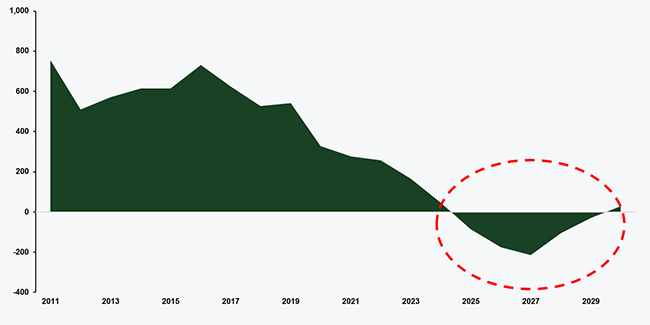

Apartment investors typically focus on assessing the propensity of younger households to rent or buy in the future. But forecasting household formation also requires monitoring demographic shifts. Green Street’s residential team assesses population growth forecasts across 12 age cohorts. For the better part of 10 years, the key renter cohort in the United States – 25- to 34-year-olds – has experienced robust population growth, representing a large, demographic tailwind backing apartment operating fundamentals. However, few market participants are focusing on the fading and ultimate reversal of this tailwind.

As today’s millennials age, population growth in this key renter cohort will see a rapid deceleration toward the turn of this decade, which will turn into absolute declines between 2025 and 2030. Ultimately, if apartment development doesn’t slow meaningfully to adjust to a dramatically different demand backdrop, these population declines could create challenging fundamentals for apartment investors.

25-34 Year Old YoY Population Growth (000's)

Supply at All-Time Highs

New supply continues to be the hot button issue for the apartment sector. Following the housing downturn, apartment construction was slow to catch up to pent-up demand, but it eventually did, and in 2016 and 2017 new supply began to weigh on landlord pricing power. Apartment construction is approaching a 40-year high in 2018.

Green Street’s residential team remains more concerned than most market participants about supply not abating for the foreseeable future, especially for apartments, and recently raised 2019 and 2020 supply growth estimates. Apartments are easier to finance than other commercial property types, and historically, apartment construction has only dropped off meaningfully during times of recession or lock-up in the capital markets.

Even though development margins are under pressure from project delays, higher construction costs, and slowing rent growth, the propensity to build is expected to continue. Developers will develop until capital shuts off. If apartment construction doesn’t moderate beyond 2018, the combination of slowing job growth, aging millennials, and stabilizing homeownership should lead to a slowdown in rent growth.

Gateway vs. Non-Gateway

Over the last 20 years, rent growth in gateway markets has outpaced non-gateway markets by roughly 150 basis points on average. While there is volatility in any given year around that average, landlord pricing power has been markedly stronger in gateway markets, defined by Green Street as San Francisco, San Jose, Los Angeles, Seattle, New York City, Washington D.C., and Boston.

However, in 2016 and 2017, non-gateway markets outperformed gateway markets, and that trend should continue this year. Stronger job growth across more affordable Sun Belt markets, restrained home buying, and above-average supply in core coastal cities helped upend this historical relationship.

Gateway markets’ relative pricing power is expected to return in 2019, though at a much narrower margin than historically. In non-gateway markets, job growth is robust but slowing, and new supply and incremental pressure toward homeownership should weigh disproportionately on rents over the next five years.

(Gateway less Non-Gateway)

Strategic Market Allocation

Green Street’s research team derives return expectations for the top 50 metropolitan areas across the major property types as part of its Real Estate Analytics offering. These market-level unlevered internal rates of return (IRRs), drawing from proprietary inputs on initial cap rates, capital expenditure requirements, and near- and long-term growth in NOI, allow investors to evaluate investment decisions across markets.

While expected returns in gateway markets are now comparable to those in non-gateway markets, that has not always been the case. Several years ago, Green Street was far more bullish on gateway markets. Many markets, including Nashville, Tampa, Austin and Orlando, have climbed the ranks, while markets like New York City have fallen. Furthermore, West Coast markets comprise an outsized share of those forecast to be the best performers. Green Street believes higher-quality job growth, coupled with relative constraints on new supply and higher barriers to homeownership, bode well for long-term apartment fundamentals in these markets.

Atlas, a new interactive commercial real estate mapping and analytics platform, is designed to help investors underwrite and compare investments across geographies and property sectors. The platform includes Green Street’s proprietary grades at the market, submarket, and zip-code level. These grades vary by sector and are based on seven variables at the zip-code level, aggregated by submarket and then by market.

Robust Private Market Demand

Several trends suggest that apartment cap rates and asset values will remain stable and are on firmer footing compared to other property types. Debt financing is widely available for apartment investors though it is more expensive with the recent rise in interest rates. The federal government (through Fannie Mae and Freddie Mac) is expected to provide ample liquidity to ensure a well-functioning apartment sector transaction market in 2018. Moreover, the private market’s affinity for multifamily investment is showing no signs of slowing. Equity providers are shifting allocations from other property types to apartments and the presence of foreign capital in the space is growing.

Disconnected Public-Private Pricing

Lately there has been a growing disconnect between the robust private market demand and the appetite for public REITs. While private market apartment asset values have climbed by ~5% in the last 12 months, apartment REITs in the public market are down ~4%, underperforming the REIT index by 450 basis points. Understanding the signals coming from the public market offers investors a competitive advantage. Significant NAV discounts, such as those currently seen for all major sectors except industrial, can be predictive of declines in private market values. Said differently, investors in the public market are far more skeptical of the outlook for asset values than their counterparts in the private market – cap rates haven’t increased, and asset prices haven’t dropped to date. For now, investors are leveraging shorter-term debt or higher loan-to-value ratios (LTVs) to make deals pencil. Additionally, lower cost sources of equity – both domestic and foreign – are offsetting rising debt costs. Should rates head higher, it seems reasonable that underwriting would adjust, and cap rates would creep up.

In spite of demographic and supply trends that bear watching, risk-adjusted returns for the apartment sector are favorable compared to all other major property types in both the public and private market. Portfolio allocations tilted toward sectors and markets offering the highest risk-adjusted return premiums should outperform. With apartment REITs currently trading at a significant discount to NAV, investors could buy a portfolio of high-quality apartments in the public market for substantially less than they would pay for physical apartment buildings through direct ownership. This disconnect provides a compelling opportunity for nimble investors able to operate in both markets.

Learn more about Green Street’s private and public market coverage of the apartment sector - including single-family rentals, manufactured housing, and student housing - via Real Estate Analytics and REIT Research.

Related Resources:

Learn more about our insights

Our thought leadership helps thousands of clients make better investment decisions every day. Inquire here to learn more about Green Street’s product suite.

More Stories

Retail Sector

Deep Dive into Local Data Company: 2023 UK Retail and Leisure Trends Analysis

Year in Review

Top U.S. News Highlights from 2023

Performance Valuation